Estimated Income – Meaning, Calculation, Taxation & Examples

What is Estimated Income?

Estimated income refers to the approximate calculation of income for a financial year before actual figures are finalized.

In simple terms:

It’s a projection of how much you will earn, used for planning taxes, advance tax payments, or financial decisions.

Where is Estimated Income Used?

Estimated income is commonly used in:

- Advance tax calculation

- Presumptive taxation schemes

- Financial planning and budgeting

- Loan applications and projections

- Business forecasting

Estimated Income in Taxation

Under the Income Tax Act, 1961, taxpayers are required to estimate their income to:

- Calculate advance tax liability

- Avoid interest and penalties

- Ensure proper tax compliance

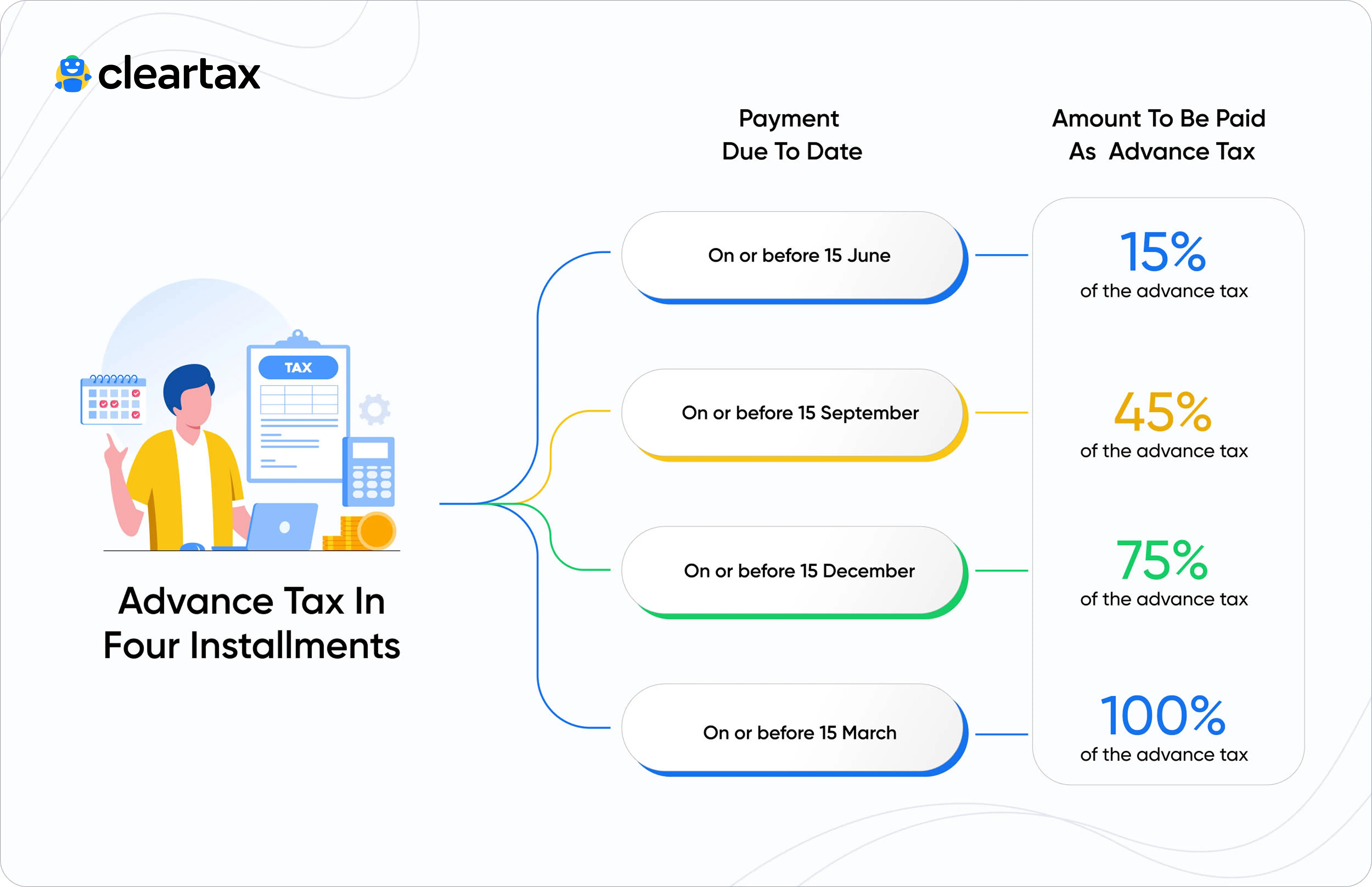

Estimated Income for Advance Tax

If your tax liability exceeds ₹10,000 in a year, you must:

- Estimate your total income

- Pay advance tax in installments

Failure to do so may result in interest under applicable provisions.

Estimated Income under Presumptive Taxation

Certain taxpayers can declare income based on estimates under sections like:

- Section 44AD (business income)

- Section 44ADA (professionals)

- Section 44AE (transport business)

In these cases:

- Income is calculated as a fixed percentage of turnover

- No detailed books of accounts are required

How to Calculate Estimated Income

Step 1: Identify Income Sources

- Salary

- Business or professional income

- Capital gains

- Interest or rental income

Step 2: Project Earnings

Estimate expected income from each source.

Step 3: Deduct Expenses & Deductions

- Business expenses

- Deductions under Section 80C, 80D, etc.

Step 4: Calculate Taxable Income

Arrive at estimated taxable income and tax liability.

Example

- Salary income: ₹8,00,000

- Interest income: ₹50,000

- Deductions: ₹1,50,000

Estimated taxable income:

₹8,50,000 – ₹1,50,000 = ₹7,00,000

Importance of Estimated Income

1. Better Tax Planning

Helps optimize deductions and reduce tax burden.

2. Avoid Penalties

Ensures timely advance tax payments.

3. Financial Planning

Supports budgeting and investment decisions.

4. Business Decision Making

Helps in forecasting profits and expenses.

Common Mistakes in Estimating Income

- Ignoring additional income sources

- Underestimating income to reduce tax

- Not revising estimates during the year

- Missing capital gains or bonus income

Key Points to Remember

- Estimated income is not final income

- It should be reviewed periodically

- Accuracy helps avoid tax notices

- Required for advance tax compliance

Conclusion

Estimated income is a crucial concept for effective tax and financial planning. A realistic estimate ensures timely tax payments, better compliance, and smarter financial decisions.